what is financial management?

“Financial management is the activity concerned with planning, raising, controlling and administering of funds used in the business.”

Financial management is that area of business management devoted to a judicious use of capital and a careful selection of the source of capital in order to enable a spending unit to move in the direction of reaching the goals.

Financial management is an organic function of any business. Any organization needs finances to obtain physical resources, carry out the production activities and other business operations, pay compensation to the suppliers, etc. There are many theories around financial management:

- Some experts believe that financial management is all about providing funds needed by a business on terms that are most favorable, keeping its objectives in mind. Therefore, this approach concerns primarily with the procurement of funds which may include instruments, institutions, and practices to raise funds. It also takes care of the legal and accounting relationship between an enterprise and its source of funds.

- Another set of experts believe that finance is all about cash. Since all business transactions involve cash, directly or indirectly, finance is concerned with everything done by the business.

- The third and more widely accepted point of view is that financial management includes the procurement of funds and their effective utilization. For example, in the case of a manufacturing company, financial management must ensure that funds are available for installing the production plant and machinery. Further, it must also ensure that the profits adequately compensate the costs and risks borne by the business.

nature of financial management

(i) Financial management is a specialized branch of general management, in the present-day-times. Long back, in traditional times, the finance function was coupled, either with production or with marketing; without being assigned a separate status.

(ii) Financial management is growing as a profession. Young educated persons, aspiring for a career in management, undergo specialized courses in Financial Management, offered by universities, management institutes etc.; and take up the profession of financial management.

(iii) Despite a separate status financial management, is intermingled with other aspects of management. To some extent, financial management is the responsibility of every functional manager. For example, the production manager proposing the installation of a new plant to be operated with modern technology; is also involved in a financial decision.

Likewise, the Advertising Manager thinking, in terms of launching an aggressive advertising programme, is too, considering a financial decision; and so on for other functional managers. This intermingling nature of financial management calls for efforts in producing a coordinated financial system for the whole enterprise.

(iv) Financial management is multi-disciplinary in approach. It depends on other disciplines, like Economics, Accounting etc., for a better procurement and utilisation of finances.

For example, macro-economic guides financial management as to banking and financial institutions, capital market, monetary and fiscal policies to enable the finance manager decide about the best sources of finances, under the economic conditions, the economy is passing through.

Micro-economics points out to the finance manager techniques for profit maximisation, with the limited finances at the disposal of the enterprise. Accounting, again, provides data to the finance manager for better and improved financial decision making in future.

(v) The finance manager is often called the Controller; and the financial management function is given name of controllership function; in as much as the basic guideline for the formulation and implementation of plans-throughout the enterprise-come from this quarter.

The finance manager, very often, is a highly responsible member of the Top Management Team. He performs a trinity of roles-that of a line officer over the Finance Department; a functional expert commanding subordinates throughout the enterprise in matters requiring financial discipline and a staff adviser, suggesting the best financial plans, policies and procedures to the Top Management.

In any case, however, the scope of authority of the finance manager is defined by the Top Management; in view of the role desired of him- depending on his financial expertise and the system of organizational functioning.

(vi) Despite a hue and cry about decentralisation of authority; finance is a matter to be found still centralised, even in enterprises which are so called highly decentralised. The reason for authority being centralised, in financial matters is simple; as every Tom, Dick and Harry manager cannot be allowed to play with finances, the way he/she likes. Finance is both-a crucial and limited asset-of any enterprise.

objective of financial management

In organizations, managers in an effort to minimize the costs of procuring finance and using it in the most profitable manner, take the following decisions:

Investment Decisions: Managers need to decide on the amount of investment available out of the existing finance, on a long-term and short-term basis. They are of two types:

- Long-term investment decisions or Capital Budgeting mean committing funds for a long period of time like fixed assets. These decisions are irreversible and usually include the ones pertaining to investing in a building and/or land, acquiring new plants/machinery or replacing the old ones, etc. These decisions determine the financial pursuits and performance of a business.

- Short-term investment decisions or Working Capital Management means committing funds for a short period of time like current assets. These involve decisions pertaining to the investment of funds in the inventory, cash, bank deposits, and other short-term investments. They directly affect the liquidity and performance of the business.

Financing Decisions: Managers also make decisions pertaining to raising finance from long-term sources (called Capital Structure) and short-term sources (called Working Capital). They are of two types:

- Financial Planning decisions which relate to estimating the sources and application of funds. It means pre-estimating financial needs of an organization to ensure the availability of adequate finance. The primary objective of financial planning is to plan and ensure that the funds are available as and when required.

- Capital Structure decisions which involve identifying sources of funds. They also involve decisions with respect to choosing external sources like issuing shares, bonds, borrowing from banks or internal sources like retained earnings for raising funds.

Dividend Decisions: These involve decisions related to the portion of profits that will be distributed as dividend. Shareholders always demand a higher dividend, while the management would want to retain profits for business needs. Hence, this is a complex managerial decision.

Long-Term Sources of Finance

Long-term financing means capital requirements for a period of more than 5 years to 10, 15, 20 years or maybe more depending on other factors. Capital expenditures in fixed assets like plant and machinery, land and building, etc of business are funded using long-term sources of finance. Part of working capital which permanently stays with the business is also financed with long-term sources of funds. Long-term financeing sources can be in the form of any of them:

- Retained Earnings or Internal Accruals

- Debenture / Bonds

- Term Loans from Financial Institutes, Government, and Commercial Banks

- Venture Funding

- Asset Securitization

- International Financing by way of Euro Issue, Foreign Currency Loans, ADR, GDR, etc.

introductory idea about capitalization

Capitalization comprises of share capital, debentures, loans, free reserves,etc. Capitalization represents permanent investment in companies excluding long-term loans. Capitalization can be distinguished from capital structure. Capital structure is a broad term and it deals with qualitative aspect of finance. While capitalization is a narrow term and it deals with the quantitative aspect.

Capitalization is the recordation of a cost as an asset, rather than an expense. This approach is used when a cost is not expected to be entirely consumed in the current period, but rather over an extended period of time.

What it is:

In the business world, capitalization has two meanings. The first meaning, also called market capitalization, refers to the value of a company’s outstanding shares. The formula for market capitalization is:

Market Capitalization = Current Stock Price x Shares Outstanding

It is important to note that market cap is not the same as equity value, nor is it equal to a company’s debt plus its shareholders’ equity (although that too is sometimes referred to as simply the company’s capitalization).

The second meaning of the term relates to the act of accounting for a cost as an asset instead of an expense.

Capitalization reflects the theoretical value of a company, but this is usually not what the company could be purchased for in a normal merger transaction. One reason for this is that the value of material nonpublic information, management changes, operating synergies between the acquirer and the company, and other intangible factors may not be reflected in the stock price or the financial statements.

Capital structure

Capital Structure refers to the amount of debt and/or equity employed by a firm to fund its operations and finance its assets. The structure is typically expressed as a debt-to-equity or debt-to-capital ratio.

Debt and equity capital are used to fund a business’ operations, capital expenditures, acquisitions, and other investments. There are tradeoffs firms have to make when they decide whether to raise debt or equity and managers will balance the two try and find the optimal capital structure.

Optimal capital structure

The optimal capital structure of a firm is often defined as the proportion of debt and equity that result in the lowest weighted average cost of capital (WACC) for the firm.

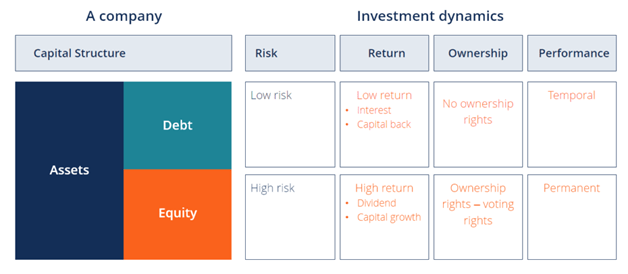

Dynamics of debt and equity

Below is an illustration of the dynamics between debt and equity from the view of investors and the firm.

dynamics of debt and equity on capital structure

Debt investors take less risk because they have the first claim on the assets of the business in the event of bankruptcy. For this reason, they accept a lower rate of return, and thus the firm has a lower cost of capital when it issues debt compared to equity.

Equity investors take more risk as they only receive the residual value after debt investors have been repaid. In exchange for this risk equity investors expect a higher rate of return and therefore the implied cost of equity is greater than that of debt.

Cost of capital

A firm’s total cost of capital is a weighted average of the cost of equity and the cost of debt, known as the weighted average cost of capital (WACC).The formula is equal to:

WACC = (E/V x Re) + ((D/V x Rd) x (1 – T))

Where:

E = market value of the firm’s equity (market cap)

D = market value of the firm’s debt

V = total value of capital (equity plus debt)

E/V = percentage of capital that is equity

D/V = percentage of capital that is debt

Re = cost of equity (required rate of return)

Rd = cost of debt (yield to maturity on existing debt)

T = tax rate

Importance of Cost of Capital

- It helps in evaluating the investment options, by converting the future cash flows of the investment avenues into present value by discounting it.

- It is helpful in capital budgeting decisions regarding the sources of finance used by the company.

- It is vital in designing the optimal capital structure of the firm, wherein the firm’s value is maximum, and the cost of capital is minimum.

- It can also be used to appraise the performance of specific projects by comparing the performance against the cost of capital.

- It is useful in framing optimum credit policy, i.e. at the time of deciding credit period to be allowed to the customers or debtors, it should be compared with the cost of allowing credit period.

Cost of capital is also termed as cut-off rate, the minimum rate of return, or hurdle rate.

Explicit cost of capital:

It is the cost of capital in which firm’s cash outflow is oriented towards utilisation of capital which is evident, such as payment of dividend to the shareholders, interest to the debenture holders, etc.

Implicit cost of capital:

It does not involve any cash outflow, but it denotes the opportunity foregone while opting for another alternative opportunity.

To cover the cost of raising funds from the market, cost of capital must be obtained. It helps in assessing firm’s new projects because it is the minimum return expected by the shareholders, lenders and debtholders for supplying capital to the business, as a consideration for their share in the total capital. Hence, it establishes a benchmark, which must be met out by the project.

Cost of debt

A company’s cost of debt is the effective interest rate a company pays on its debt obligations, including bonds, mortgages, and any other forms of debt the company may have. Because interest expense is deductible, it’s generally more useful to determine a company’s after-tax cost of debt. Cost of debt, along with cost of equity, makes up a company’s cost of capital.

Calculating cost of debt

In order to calculate a company’s cost of debt, you’ll need two pieces of information: the effective interest rate it pays on its debt and its marginal tax rate.

Many companies publish their average debt interest rate, but if not, it’s fairly easy to calculate using the company’s financial statements. On the income statement, you can find the total interest the company paid (note: If you’re looking at a quarterly income statement, multiply this figure by four in order to annualize the data). Then, on the balance sheet, you can find the total amount of debt the company is carrying. Divide the annual interest by total debt and then multiply the result by 100, and you’ll get the effective interest rate on the company’s debt obligations.

Keep in mind that this isn’t a perfect calculation, as the amount of debt a company carries can vary throughout the year. If you’d like a more reliable result, then you can use the average of the company’s debt load from its four most recent quarterly balance sheets.

Next, determine the company’s marginal tax rate (federal and state combined). For most large corporations, the federal marginal tax rate is 35%, as this rate applies to all income over $18.33 million. State corporate income taxes range from 0% to 12% as of 2016.

Finally, to calculate the after-tax cost of debt, simply subtract the company’s marginal tax rate from one and then multiply the result by the effective tax rate you found earlier.